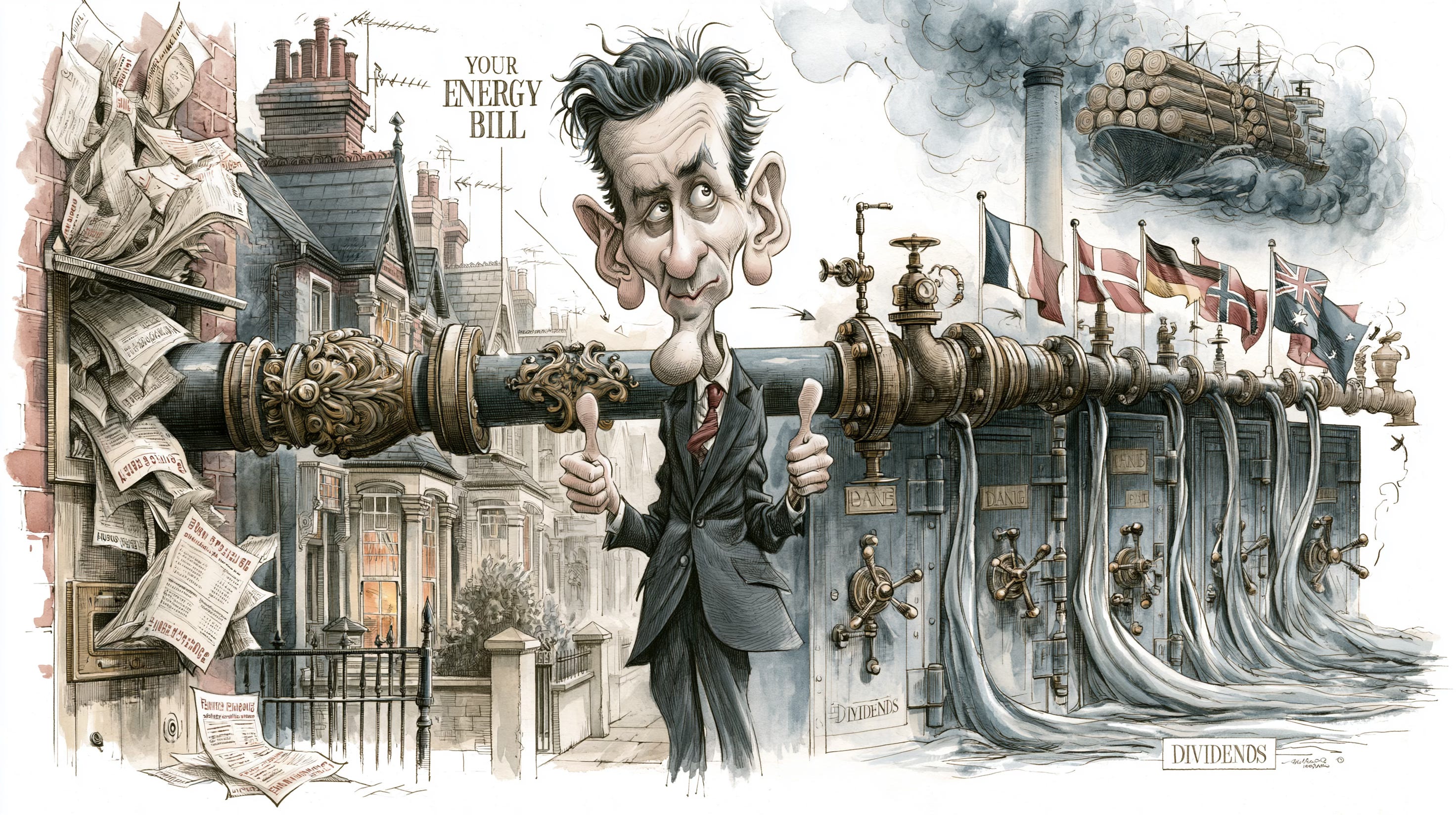

Your Bills. Their Dividends.

Part Two: The money left your bill and went to Copenhagen, Paris, Frankfurt, Beijing — and a power station burning wood imported from America.

Series Introduction

In 2008 a law was passed without the courtesy of disclosing its costs. Domestic gas production was quietly run down in the name of energy security. Import dependency grew. Bills rose. The borrowing required to fund the transition helped push up mortgage rates. Levies multiplied. Billions in subsidies flowed smoothly into the accounts of foreign shareholders. And each crisis this machinery produced was immediately presented, with an almost touching consistency, as conclusive proof that the policy must accelerate — more spending, more borrowing, more levies, more contracts, and more foreign dividends. The next crisis duly arrived. The same argument was made again, with undiminished sincerity.

The policy creates the crisis. The crisis justifies the policy. It is a perfect, self-reinforcing loop. The same men who built the machine are still running it, still explaining it to the public, and still quietly filing away the letters that once inconveniently calculated what it would cost.

Three articles. One mechanism. Every dot now connected — from the 2008 vote to your energy bill, your mortgage, your rent, your weekly shop, the foreign hands collecting the returns, and the case for repealing Net Zero.

The dots have always been in the public record. Until now, nobody has connected them.

Part One had the courtesy to name the system and the gentlemen who, with such touching diligence, constructed it. The question of where the money actually goes, however, yields answers that are pleasingly specific, exhaustively documented and, in several of the more instructive cases, pleasingly foreign. What follows is not ministerial abstraction but a tracing of the funds themselves.

The contract Ed Davey concluded with EDF — dissected in Part One — remains the neatest illustration of how the apparatus recoups its outlay. Yet Hinkley Point C is merely one agreement among many, and EDF merely one overseas beneficiary among several. The complete ledger is considerably larger, far less reported and altogether more expensive than any single contract would imply.

Orsted, the Danish state-backed enterprise, has erected nearly six gigawatts of generation capacity in British waters — roughly six times what it has managed in its own territorial waters.

One might be forgiven for imagining this reflects some profound climatic zeal, in reality it reflects the Contracts for Difference mechanism, which, as one market analysis has observed with admirable restraint, offers the ultimate safe bet, a captive market of 67 million souls who cannot decline electricity and who will pay the price their own government has statutorily guaranteed.

RWE is German. Vattenfall is Swedish and state-owned. Equinor — Norway’s state energy company, the same Norway whose sovereign wealth fund now exceeds £1 trillion and whose households were largely insulated from the 2021-22 gas price spike — cheerfully collects British CfD subsidies through its UK offshore wind portfolio while simultaneously selling Britain the liquefied natural gas it can no longer produce for itself.

The same country appears on both sides of Britain’s energy dependency. One notes this without further elaboration.

Macquarie, the Australian investment colossus now proposing 2,500 acres of solar panels in Norfolk — with compulsory acquisition for any landowner indelicate enough to demur — is present for precisely the same reason. The gas pipes and power grids themselves are largely in the hands of investors from Canada, Qatar, Hong Kong, Bermuda and the Cayman Islands.

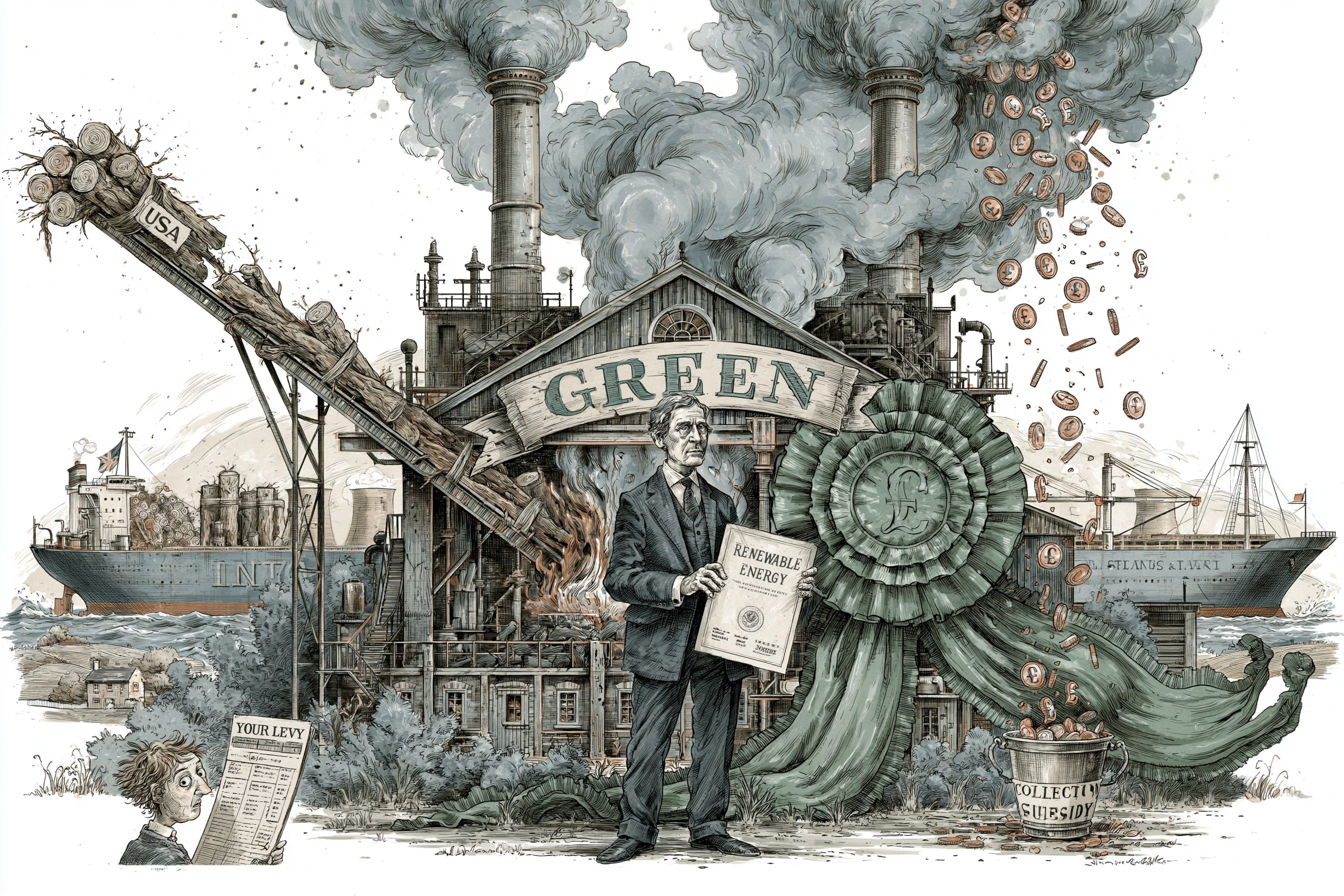

Then there is Drax. Unlike the foreign state enterprises listed above, Drax Power Station in North Yorkshire is British-listed. What it has done with British household levy payments is, if anything, more instructive than anything its overseas counterparts have managed.

Since converting from coal to biomass — compressed wood pellets imported from forests in the United States and Canada — Drax has received more in renewable energy subsidies than any other company in British history. By 2025 the annual subsidy payment stood at approximately £999 million, collected through household energy levies, paid to a company to import wood from North America and burn it.

The government classifies this as renewable energy. The Climate Change Committee, the Royal Society of Chemistry and a growing body of scientific opinion have questioned whether it reduces carbon emissions at all when the full lifecycle is examined. The subsidy continues regardless. The wood pellets cross the Atlantic. The levy leaves your bill. The dividend reaches the shareholder.

A think-tank analysis records that energy networks and generation companies have disbursed £70.7 billion in dividends since 2010. That sum originated as a statutory levy on British household energy bills. It concluded its journey as dividend cheques dispatched to shareholders in Copenhagen, Paris, Frankfurt and Beijing.

Britain, in the sacred name of “energy security”, dismantled much of its domestic gas production and substituted a subsidy architecture expressly engineered to transfer household payments to foreign state enterprises, overseas investment funds and British-listed companies burning imported wood — guaranteed by statute, impervious to electoral outcomes and contracted to run for decades.

If a more comprehensive inversion of a declared policy objective exists in the annals of British public administration, we have yet to encounter it.

Yet the energy bill is merely the most visible conduit. The machine delineated in Part One does not restrict its exactions to a single quarterly statement. It transmits them, through specific and traceable channels, into almost every financial obligation a British household assumes, the mortgage, the rent, the weekly shop, the new car, the cost of acquiring a home.

Each possesses a statutory address. None arrived with an explanatory note.

The Energy Bill: The relief that the contracts do not permit

Most householders still cling to the quaint notion that their energy bill rises when gas grows dear and falls when it grows cheap. This is true of one solitary component. The remainder operates on principles that have nothing whatever to do with wholesale gas prices and everything to do with the statutory machine.

Three charges are embedded in every British household energy bill that are structurally immune to market movements. They did not rise because Russia invaded Ukraine. They will not fall when peace, in due course, breaks out. In the exquisitely measured language of regulatory determination, they are locked in.

Ofgem’s RIIO-3 network charge adds £66 per household annually, already baked into the 2026 price cap to fund the grid upgrades demanded by mass electrification, and scheduled for an upward review in 2028. It applies with serene indifference whether gas costs £1 or £100 per unit.

The Contracts for Difference portfolio guarantees renewable generators a fixed above-market price for electricity for up to fifteen years — obligations cheerfully signed when wholesale prices were lower, running merrily on to 2038 and beyond, and curiously immune to renegotiation when market conditions improve.

The capacity market, meanwhile, pays conventional gas stations to remain on standby for every hour that intermittent renewables cannot be prevailed upon to deliver. The consumer therefore funds both the renewable generation and the gas generation kept idling in case the renewables prove temperamentally uncooperative.

In April 2026 the government moved 75 per cent of the Renewables Obligation cost off household bills and into general taxation — a reduction of approximately £134 for a typical household. The Contracts for Difference obligations, the network charges and the capacity market costs remain.

Two complete generation systems. One bill.

Now consider what happens when wholesale gas prices do, periodically, fall — as they have a tiresome habit of doing — and a minister steps forward with the air of a man revealing a state secret to announce that households should expect relief on their energy bills.

That minister either knows, or ought to know, that the Contracts for Difference running to 2038 legally prevent the full benefit of any such fall from reaching the consumer. The network charges remain fixed by regulatory fiat regardless of market conditions. The capacity-market costs, far from shrinking, expand as the renewable fleet itself expands. The floor does not move. The announcement is made anyway.

This is not incompetence. It is the system performing exactly as the series introduction described — presenting the damage as something other than what it is, on behalf of the very people who built the damage and are still, with undiminished enthusiasm, running it.

The money, in the meantime, flows abroad. And that is the part of the energy bill that has received the least attention of all.

The Mortgage: A statutory component your broker forgot to mention

The net-zero transition demands tens of billions in annual public spending, grid upgrades, subsidy mechanisms, the Warm Homes Plan, public-sector decarbonisation and the ever-expanding administrative apparatus of compliance across housing, transport and industry. All of it is financed through gilt issuance — that is, government borrowing — adding permanently to the structural deficit long before any geopolitical crisis deigns to intervene.

More gilts in the market mean more supply. More supply means higher yields — the interest rate at which the government borrows. The ten-year gilt yield sank to a scarcely believable 0.3 per cent at its pandemic nadir. It has spent much of 2025 and 2026 comfortably above 4.5 per cent. Net Zero borrowing is not the only upward pressure on that figure. It is, however, a permanent, statutory and relentlessly compounding one.

Fixed-rate mortgage pricing in Britain tracks swap rates, which in turn track gilt yields. A yield elevated in part by Net Zero borrowing by a mere fifty basis points above where it would otherwise sit translates, on a £250,000 repayment mortgage over twenty-five years, to roughly £70 extra per month — or £840 per year. Every year. For the entire life of the mortgage.

The Bank of England tightens the screw still further. A significant portion of domestic inflation is now structural rather than cyclical — embedded in levy floors and statutory mandates whose origins lie in Acts of Parliament rather than mere market demand.

The Bank cannot cut rates as freely as a slowing economy might otherwise warrant, lest it disturb a price level whose floor is set not by economic conditions but by political decree. Rate reductions are therefore more modest than the economic data alone would appear to justify.

Consider the household remortgaging this year — one of roughly one million doing so in 2026 — discovering that its monthly payment is several hundred pounds higher than when it last fixed in 2021.

A traceable, documented and thoroughly statutory component of that increase is the Seventh Carbon Budget, laid before Parliament in February 2025 without any cost-benefit analysis being distributed to the people expected to pay for it, and without the serious parliamentary discussion that Peter Lilley had been politely requesting since 2009.

Their lender did not mention this. Their mortgage broker did not mention this.

The Rent: Nineteen years of paying for something you cannot have

Consider two neighbours on the same unremarkable street. One owns his home. One rents. Both pay identical energy bills and are subject to precisely the same statutory levies — the RIIO-3 charge, the Contracts for Difference costs, the capacity-market payments — at the same flat rate per unit consumed. Income, tenure and circumstance are, as far as the levy is concerned, irrelevant.

The homeowner is eligible for a heat-pump grant of up to £7,500, funded in part by the very levy both neighbours pay. The tenant is not. The property is not his. The grant is, in the elegant bureaucratic phrase, structurally inaccessible.

The average annual energy levy paid by a household is approximately £400. At that rate the tenant will have contributed the equivalent of one such grant after nineteen years — nineteen years of dutifully funding a subsidy he can never claim.

As the levy rises — and it will — the nineteen years extends. The tenant does not approach the grant. The grant moves away.

Nineteen years. This is not policy in the abstract. It is the distributional reality of Net Zero expressed as a cold, clarifying number.

The Resolution Foundation has documented the effect. The Joseph Rowntree Foundation has documented it. The wealthiest fifth of British households are roughly four times more likely to own their own home than the poorest fifth.

The grants therefore flow upwards. The levies remain flat. The policy tirelessly sold as the great progressive project of our age is, when one follows the actual cash, a reverse Robin Hood — conducted through energy bills, at statutory scale, and in full view of anyone with the impertinence to examine the figures.

Nor does the burden end there. Net Zero is also quietly raising the tenant’s rent through two additional mechanisms. Minimum Energy Efficiency Standards compel landlords to retrofit properties to ever-tighter specifications. Costs are recovered either through higher rents or by the landlord exiting the market altogether — both outcomes rather disagreeable for the tenant.

The landlord who complies passes on the bill. The landlord who withdraws removes supply and pushes rents higher across what remains. Meanwhile, the Future Homes Standard adds an average £4,350 to every new dwelling, rendering marginal development sites unviable, constraining supply in an already desperately short market, and lifting rents across the entire existing stock as a result.

The tenant did not vote for the Energy Performance of Buildings Regulations. He was not consulted on the Future Homes Standard. Yet he pays for both — through his rent, through his levy, and through nineteen long years of grants he will never see.

The Food Shop: Made in Westminster, paid at the till

Two quiet mechanisms link Net Zero legislation to the price of the weekly shop — neither of which has ever troubled the mainstream coverage of food-price inflation.

The Environmental Land Management schemes have already diverted millions of hectares of British farmland from the prosaic business of growing food to the more fashionable pursuits of woodland creation, peat restoration and energy crops. Government projections suggest the proportion affected will reach roughly ten per cent by 2030.

The National Farmers Union has warned that farmers are being forced to scale back food production as a direct consequence — and has called, so far without success, for Defra to publish an impact assessment of what ELM schemes are actually doing to domestic food output.

The irony here is particularly exquisite, British farmland is being taken out of food production in order to grow energy crops, while British households continue to pay above-market rates for electricity generated by foreign-owned wind farms under government-guaranteed contracts. The land yields less food. The energy arrives from abroad. The household, with admirable impartiality, funds both.

Reduced domestic supply naturally means greater reliance on imports and food prices more vulnerably exposed to the caprices of global commodity markets. The effect settles gently, almost apologetically, alongside every other cost alighting on the same household at once.

Then there is the second, less discussed, pressure. UK industrial energy costs are the highest of any IEA member nation — confirmed by DESNZ data and running at 125 per cent above the EU median for large industrial users, a direct and thoroughly documented consequence of the carbon pricing and levy architecture described in this series.

Food processing, cold storage, packaging, distribution, every stage of the supply chain from field to supermarket shelf carries an embedded energy cost premium that competitor economies, unburdened by equivalent statutory enthusiasm, simply do not bear.

The ONS confirmed food price inflation reached 19.1 per cent in March 2023, with energy costs among the primary drivers. That cost does not announce itself at the checkout. It distributes itself, with commendable discretion, across every item in the basket. When anyone attributes it at all, it is solemnly blamed on global commodity pressures.

It is, in a traceable and statutory part, nothing of the sort. It is a domestic policy choice.

Made in Westminster. Paid at the till. By every household in Britain, every week, without the courtesy of an explanation.

The Car: The tax that does not appear on the invoice

The Zero Emission Vehicle Mandate requires that 33 per cent of new cars sold this year must be zero-emission. Miss the target and manufacturers face a penalty of £12,000 for every non-compliant vehicle — a sum so elegantly calibrated that it creates an immediate and overwhelming incentive to recover the costs somewhere else.

In 2025, manufacturers collectively offered £10 billion in discounts on electric vehicles — an average of £11,000 per car — in order to drive demand and meet their mandate targets, according to figures from the Society of Motor Manufacturers and Traders.

That £10 billion has to be recovered somewhere. It is being recovered from the buyers of conventional vehicles. The Volkswagen Group’s UK sales director confirmed as much at the SMMT’s Electrified conference in March 2026, the discounting is unsustainable and the cost of conventional vehicles will rise significantly as manufacturers recoup their losses.

He did not, of course, mention this to the buyers of those conventional vehicles. Neither did anyone else.

Some manufacturers have taken a more direct approach, rather than discounting EVs further, Stellantis — owner of Vauxhall, Peugeot and Citroën — restricted the supply of conventional vehicles to the UK market, making them artificially scarce and pushing buyers toward electric alternatives.

The mandate, in other words, does not merely transfer costs invisibly. It can also restrict the choice of the buyer who declines to make the approved one. Every family purchasing a petrol hatchback this year therefore pays a premium — unitemised, unannounced and entirely invisible on the invoice — that subsidises the electric vehicle their neighbour may or may not have chosen.

Every tradesman financing a diesel van finds himself cross-subsidising the electric fleet of a competitor who made the transition earlier.

The transfer operates at industrial scale across every forecourt in Britain.

A buyer of a new car enjoys the statutory right to know the interest rate on his finance agreement to four decimal places. He enjoys no equivalent right to know how much of the sticker price is actually a government-mandated compliance levy. One disclosure is required by law. The other, curiously, is not.

It is not a voluntary contribution to a cleaner future. It is a statutory mandate, expressed through pricing, without the elementary courtesy of disclosure.

The New Home: The £4,350 they forgot to put on the poster

The Future Homes Standard adds an average £4,350 to the construction cost of every new dwelling in England — a figure graciously supplied by the government’s own regulatory impact assessment. This sum does not, as one might romantically hope, linger with the developer. It passes straight through to the buyer. Or, where it renders a site financially unviable, it ensures the home is never built at all.

For the first-time purchaser already balanced precariously at the outer limit of what today’s elevated mortgage rates permit them to borrow, that £4,350 can be the precise difference between qualifying and not qualifying. It is worth noting that the elevated mortgage rate itself is, in part, a consequence of Net Zero borrowing raising gilt yields — as we have already had occasion to observe.

The aspiring buyer therefore confronts a higher purchase price because the Standard raises build costs, and a higher borrowing cost because Net Zero raises the cost of government debt. Two outputs of the same statutory machine, arriving on the same doorstep at the same inconvenient moment. The £4,350 upfront quietly compounds into approximately £7,200 over a twenty-five-year mortgage at current rates.

It also attracts stamp duty on the inflated purchase price — a statutory tax on a statutory cost increase, compounding on the same transaction, appearing on no government poster.

The Standard also has the happy effect of rendering marginal development sites unviable — precisely those sites in the Midlands, the North and parts of the South West where development margins are thinnest and new supply is most desperately needed. In these areas the policy reduces housing supply most aggressively where affordability problems are already most acute.

The government simultaneously insists that developers meet the Future Homes Standard and then publicly scolds them for failing to build enough homes. The causal connection between these two positions has yet to feature in any ministerial statement on the housing crisis.

Fewer homes built means higher prices across the entire market — including for properties constructed long before the Standard existed and bearing no direct relation to it.

A policy that makes new homes greener for some, considerably less attainable for many, and more expensive for everyone.

The Reckoning

Assemble the pieces for both households and the picture that emerges is rather more considerable than any ministerial leaflet has ever admitted.

For the renter, an energy bill carrying three permanent statutory charges impervious to wholesale price movements, rent quietly elevated by retrofit pass-throughs and the supply constraints imposed by the Future Homes Standard, a food shop bearing an embedded industrial energy premium and the first stirrings of an agricultural supply contraction, a car payment that includes an unannounced statutory cross-subsidy, and nineteen years of levies funding grants the tenant is structurally ineligible to claim.

Approximate annual Net Zero cost across all channels, in the region of £1,500 to £2,000, depending on consumption, location and vehicle use.

For the homeowner remortgaging this year, all of the above, plus a mortgage elevated by a traceable statutory component of gilt-yield pressure, compounded by a central bank that finds itself politely constrained from cutting rates by the very inflation floors Parliament has legislated into existence.

Approximate annual Net Zero cost across all channels, in the region of £2,500 to £3,500, depending on mortgage size, consumption and vehicle.

These figures are derived from the primary sources cited. They are conservative — they make no allowance for the full forward trajectory as electrification deepens, Contracts for Difference obligations expand and the network levy marches towards its 2028 review.

Each cost has a statutory address. Each was decided in Parliament. Each sits in the public record.

None of it was in the leaflet.

What was in the press release instead was the declaration that the very costs documented above constitute irrefutable proof that the transition must accelerate. More spending. More borrowing. More levies. More contracts guaranteed to foreign generators. The damage, in other words, is being recycled in real time into the justification for more of the same policy. The loop is not a conspiracy theory. It is the sequence of events described across the first two articles, running precisely on schedule.

The question Article Two cannot answer is the one that matters most. If this is what continuing costs — traced, documented and statutory — then what, precisely, does stopping cost? The repeal movement has not said. The government has not published it. The figure has never been calculated in public.

Article Three calculates it. The answer will surprise those calling loudest for repeal rather more than it surprises anyone else.

On the 1st June Labour released the 2nd batch of papers associated with the Mandelson affair. Some of the requested materials were retained on 'security grounds'.

The balance of those papers delivered 3 months late was grim, vile, grubby, and utterly corrupt.

Then I read this.

Mr E Miliwatt, Chef D'Mission Stark and the CCC should be suspended immediately, and then fired the very next day.

Following that there should be full disclosure of all contacts, all investments, every single penny they've handled. All have lost their 'right' to privacy. There's grift, and it needs to be removed.

Oh, and that does include the current leader of the Lib-Dems (Post Office scandal and this - minister at the time in both cases - yet apparently knew nothing about anything).

The thing is it’s not that you haven’t got an argument, it’s that they can’t allow themselves to think that you might have an an argument.

There is a saying that you can wake someone who is asleep, but you can’t wake someone who is pretending to be asleep.

My cousin who is in her 90s often discusses Question Time and other political debates. Recently when the debates surrounding the Welsh Assembly were on I discussed energy policy with her and said I would only vote for a party which would get rid of the net zero law. She said that if it was that important everybody would be talking about it. She voted for one of the legacy parties - the same one she usually votes for.

I’m afraid we’ll have to wait until the grid goes down or we can’t borrow any more money before people open their eyes.